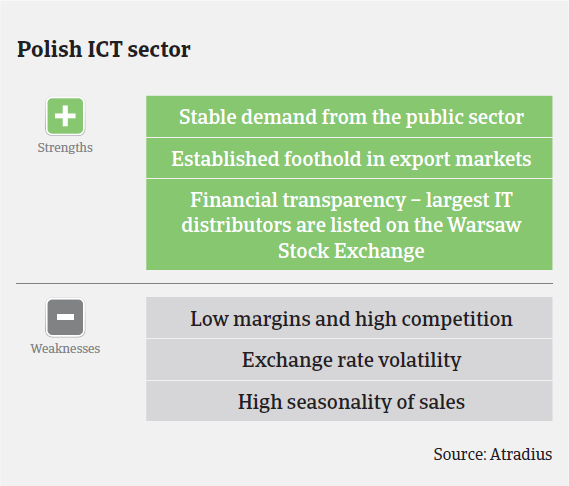

The main strengths of the Polish IT sector are the stable demand, a strong export performance and financial transparency, as the largest IT distributors are listed on the Warsaw Stock Exchange.

Poland

- Good growth prospects in the medium term

- Fierce competition and low margins remain challenges

- Stable payment behaviour expected

The Polish IT sector is mainly divided into three segments: hardware (which accounted for 41% of sales in 2014), software (18%) and IT services (41%). Last year the Polish IT market grew 3% to PLN 29.7 billion according to BMI Research. Poland remains the most attractive IT market in Central and Eastern Europe. After strong double-digit growth rates before the 2008 credit crisis, annual growth rates have decreased to between 3% and 7%.

In 2015, IT market growth is forecast to slow down to 2.4%. Computer hardware spending is expected to decrease as businesses’ hardware upgrade spending was boosted by Microsoft’s withdrawal of support for the legacy XP operating system in April 2014, which brought forward demand from 2015. The tablet boom is expected to lose some momentum after strong sales in 2013 and 2014. An area of the hardware market where we envisage stronger performance in 2015 is low-cost notebooks and hybrid notebooks.

The IT software and services segments are expected to grow 3.4% and 4.3% respectively in 2015, with demand underpinned by rising business confidence. The telecommunication, financial services, and retail sectors in Poland all offer significant growth opportunities in 2015 as enterprises look for cost-saving and capacity-increasing IT products and solutions. There are specific opportunities in the healthcare segment as the government presses forward with the computerisation of hospitals and other health facilities.

The main strengths of the Polish IT sector are the stable demand from the public sector, a strong export performance and financial transparency, as the largest IT distributors are listed on the Warsaw Stock Exchange (WSE). IT services benefit from steady demand from sectors such as healthcare and financial services.

Despite good medium-term prospects, the Polish IT sector is affected by exchange rate volatility, seasonality of sales, fierce competition and low margins. The largest players continue to record rising sales revenues and increasing profits, made possible by the high volume of sales (which enable them to offer competitive prices) and increasing exports. For example, in the IT distribution segment three large players (AB SA, ABC Data SA and Action SA) hold together a market share of more than 75%. Those three players are increasingly taking over smaller distributors’ market shares and entering other, higher-margin sectors (like toys in the case of AB SA).

It is common in the Polish IT sector that many companies have a low net worth, and solvency very often does not exceed 25% (the situation is even more serious for system integrators with very high seasonality).

Due to very high competition, the level of profitability rarely exceeds 2%. The whole sector has to deal with low margins and focus on cutting costs. Liquidity is very often strained. It is characteristic for this sector that companies have a diversified portfolio of contractors and change their suppliers very often.

Our underwriting approach towards the IT sector can be described as neutral to positive. Insolvencies and payment delays are not expected to increase in 2015. The three biggest players in the IT distribution segment are all quoted on the WSE, and are highly rated and transparent in their actions. However, smaller players have to be monitored more closely. Low margins, fast growth, insufficient management and controlling quality are all indicators that may indicate problems.

関連ドキュメント

1MB PDF