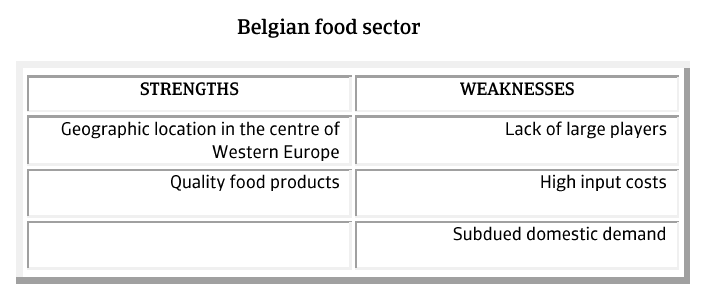

Exports are increasingly more important for the Belgian food sector, with Europe, mainly the Netherlands as the largest market.

Belgium

- Russian import ban could lead to more insolvencies

- Margins under pressure from high labour and energy costs

- Falling raw material prices have a positive impact

The Belgian food sector recorded a modest 1.5% growth in turnover in 2013, to EUR 48.2 billion, driven mainly by a boost in the beverage segment (up 3.8%) and the dairy industry (up 10.6%). Exports are increasingly important for the sector, accounting for 50% of total turnover. The industry’s main subsectors are meat, oil & fats, and the segment covering chocolate, sugar, coffee and prepared meals.

The region of Flanders accounts for 80% of the food industry´s turnover, 72% of employment and 72% of the companies in the sector.

The EU remains the largest market for Belgian food exports, mainly the Netherlands (its largest market), France and Germany. Exports to the US, Japan and the BRIC countries continue to rise, with the quality and safety standards of Belgian food both key selling points.

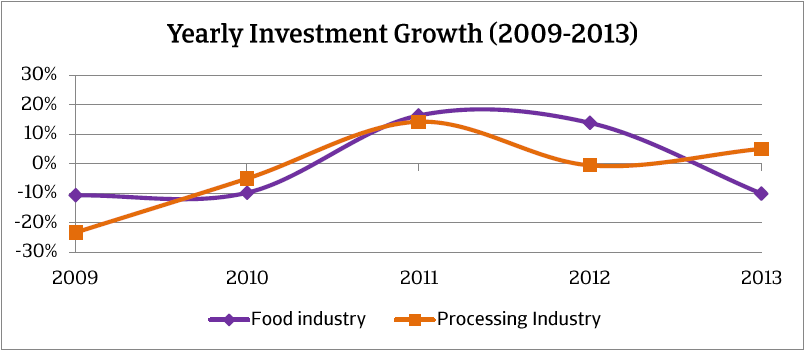

Investments should be made to ensure that the food sector increases its productivity to help cope with mounting price pressure from high domestic labour and energy costs. However, this year the Belgian food sector has invested EUR 1.16 billion in tangible fixed assets: substantially lower than in previous years. After an impressive 13.8% growth in 2012, investments fell 10.2% year-on-year in 2013. As a result, the sector’s investment intensity has dropped below that of 2009.

Belgian food companies face volatile raw material prices, which have fallen over the last six months. While this has negative consequences for farmers and growers, it creates opportunities for processing companies. Clearly it is vital to hedge against such price swings to reduce pressure on margins already narrowed by high labour and energy costs.

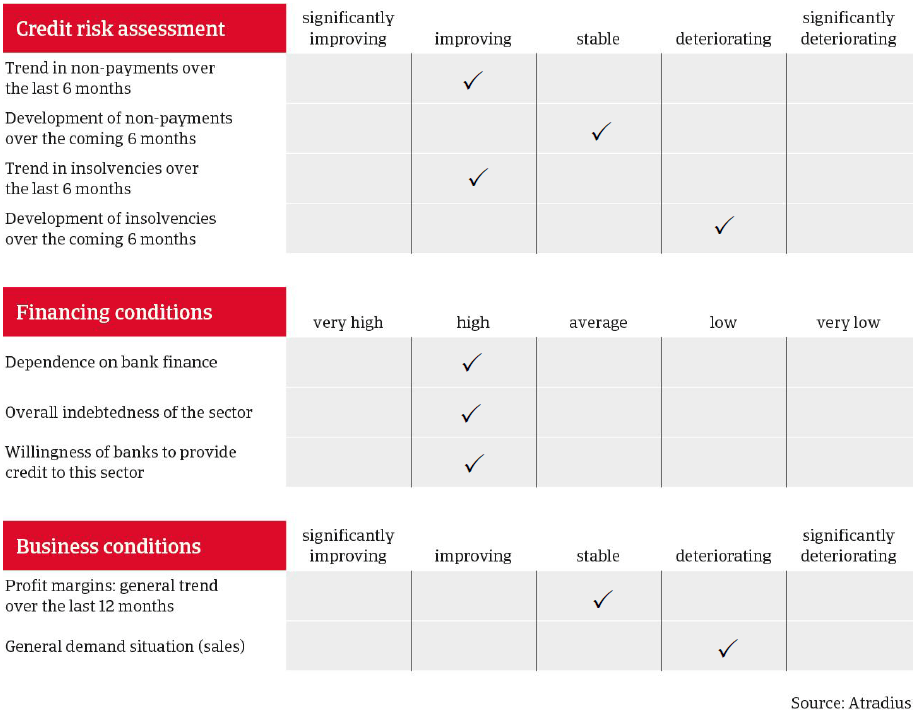

The food sector has seen an improvement in non-payment and insolvencies (74 insolvency cases between January and August this year, compared to 112 cases in the same period of 2013. However, the Russian food embargo could cause insolvencies to increase in Q4 of 2014, mainly affecting fruit & vegetable exporters. In view of these circumstances, our underwriting stance remains cautious, especially for the fruit & vegetables and the meat sector. As mentioned, volatile commodity prices, coupled with high labour and energy costs, are putting pressure on margins.

We seek the most recent available financial information on each buyer and, if possible, interim figures. Additionally, we monitor stock levels, trade creditors, debts, turnover, margins, payment delays and social security default. We also pay close attention to the evolution of raw material prices. Also important for food sector assessment is the potential for further incidents of infection and contamination, causing health issues. We take account of the seasonal trends that affect most food subsectors and manage credit exposure through time-limited cover. Despite our general cautious stance, we always try to find ways to maximise cover by obtaining additional information on, for instance, good payment experience or a guarantee from a stronger parent company.

関連ドキュメント

3.45MB PDF