The machinery sector should benefit from the economic rebound in France, with GDP forecast to grow 1.1% in 2015 (after 0.2% in 2014) and stronger growth in industrial production and exports.

- Growth mainly due to automotive rebound

- Machinery businesses related to construction still carefully monitored

- Machinery insolvencies expected to level off in 2015

The French machinery sector has continued its modest rebound that started last year. Machinery production recorded 0.1% year-on- year growth in 2014 and increased 0.8% in Q1 of 2015, with inventories slightly above average. Order books have stabilised, albeit on a low level, and exports to EU markets increased. The rebound is mainly due to increased demand from automotive buyers, together with a dynamic aerospace sector.

However, machinery demand from construction still remains low, and while agricultural machinery was growing in the past, this subsector now appears to be facing some difficulties, as farming equipment buyers may reduce their investments due to lower revenues. But in general machinery should benefit from the economic rebound in France, with GDP forecast to grow 1.1% in 2015 (after 0.2% in 2014) and stronger growth in industrial production and exports.

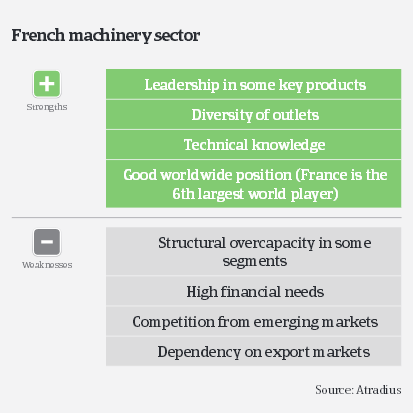

In the long term, overcapacity still remains a concern for the French machinery sector as, despite the positive trend, demand remains comparatively subdued, with limited investment from the main customer sectors. Industrial production capacities have been used at about 80% over the last two years, which implies limited investments for a large part of businesses.

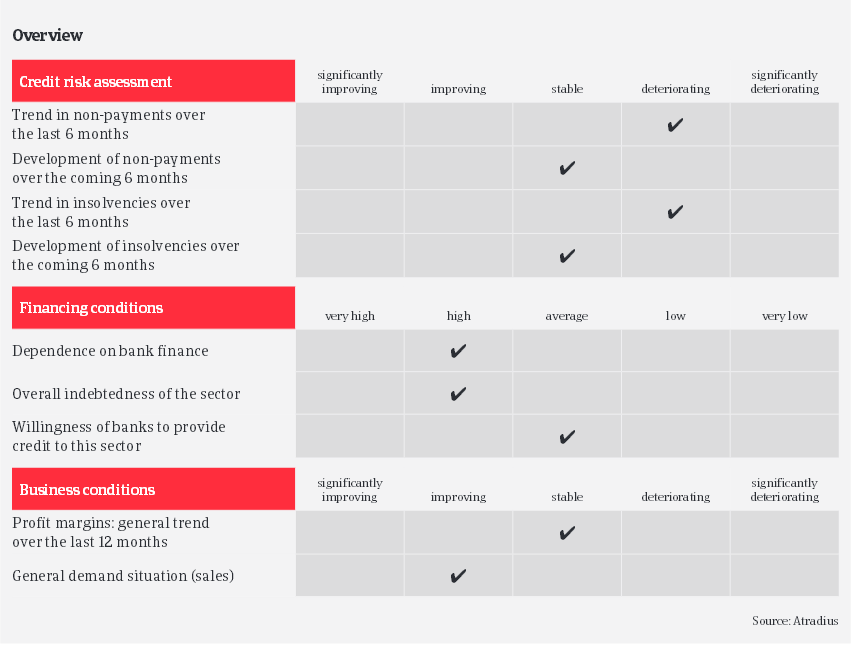

In this capital intensive industry, financing needs are high. As a result, businesses in this sector can incur large debts that weaken their financial structure and overall solvency, putting undue stress on liquidity. However, in many cases advance payments can improve suppliers’ cash situations, while banks seem willing to lend.

On average, payments in the French machinery sector take 70- 80 days. Payment delays have increased in the last six months, but no further increase is expected in the second half of 2015. Machinery insolvencies increased slightly in 2014, but are expected to level off in 2015, mainly thanks to manufacturing businesses ´ intentions to increase their machinery investments.

In view of the modest positive outlook, we have relaxed our underwriting stance, especially for small credit limit applications, although we require more information and updates of the buyer’s situation when it comes to requests for higher limits. We are still cautious on companies selling to more distressed business sectors like construction, due to the continued poor payment behaviour in this industry. Consequently we continue to carefully monitor the more distressed subsectors:

- Manufacturing of metal structures/boiler making, which has a direct link to the construction sector. We have identified the weakest companies by checking their financial commitments, margins, order books and type of construction, e.g. public works, structural works, residential or non-residential.

- Machine tools linked to the construction sector, as in this segment the production period is often very long (between 6-9 months), which implies a high need for working capital financing.

関連ドキュメント

1003KB PDF